What are common social security mistakes to avoid, learn from my own mistakes so you also don’t make the same mistakes that I did. Your retirement income depends on knowing this information, and I am more than happy to take the time to share with you.

Affiliate Disclosure

Amazon + Friends

Affiliate Disclosure: Some of the links on this website may be affiliate links. This means that if you click a link and make a purchase, I may earn a small commission at no extra cost to you. These commissions help support 65 Plus Life and Boomer Biz HQ, and Dawg Solutions. so I can continue creating free resources for older adults.

Amazon Disclosure: As an Amazon Associate, I earn from qualifying purchases. Any Amazon links used throughout this website may earn a commission when you purchase through them.

Wealthy Affiliate Disclosure: I am also a proud affiliate of Wealthy Affiliate. If you choose to join their platform through my referral link, I may earn a commission. I only recommend Wealthy Affiliate because it has personally helped me build websites and create income online, and I believe it can help other older adults learn these skills too.

Thank you for supporting my work — it truly means a lot.

Jeff

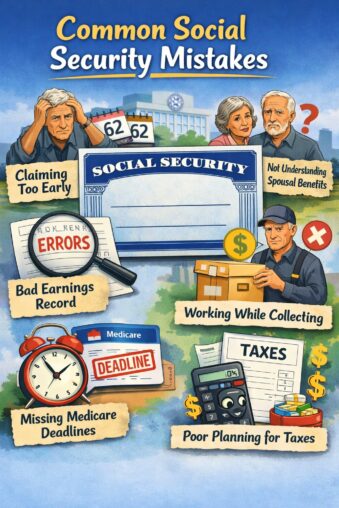

The Most Common Social Security Mistakes I’ve Made

When I first started navigating Social Security, I’ll be honest—I thought it would be simple. It wasn’t.

Looking back, I made a few mistakes that cost me money, caused confusion, and added unnecessary stress. If I can help you avoid even one of these, this article will be worth it.

Here are the biggest lessons I learned the hard way:

1. Claiming Benefits Too Early Without a Plan

One of the biggest mistakes I made was not fully understanding the long-term impact of claiming early.

Yes, it’s tempting to start at 62. I get it—I did too. But what I didn’t fully appreciate at the time was how much that permanently reduces your monthly benefit.

What I learned:

- Claiming early can reduce your benefit by up to 30%

- That reduction lasts for life

- Waiting—even a few years—can significantly increase your income

If I could do it over again, I would’ve taken more time to run the numbers and think long-term.

2. Not Understanding How Working Affects Benefits

I also didn’t realize how working while collecting Social Security could impact my payments.

At one point, I was earning income and collecting benefits—without fully understanding the earnings limits.

What happened:

- My benefits were temporarily reduced

- It caught me off guard

- I had to go back and figure out what went wrong

What I learned:

- If you’re under full retirement age, income limits apply

- Exceeding those limits can reduce your benefits

This is one of those things nobody explains clearly—until it happens.

3. Ignoring Taxes on Social Security

How Do I Handle Taxes In Retirement Revealed

This one surprised me the most.

I assumed Social Security income was tax-free. That’s not always the case.

What I learned the hard way:

- Depending on your total income, up to 85% of your benefits can be taxable

- Other income (like pensions, withdrawals, or part-time work) can push you into that zone

I didn’t plan for this early on, and it affected my overall retirement income more than I expected.

4. Not Checking My Earnings Record Early Enough

Your Social Security benefit is based on your earnings history. Sounds simple—but I didn’t verify mine until later than I should have.

The problem:

- Errors can happen

- Missing income years can lower your benefit

What I wish I had done:

- Checked my record regularly on the SSA website

- Corrected any issues early

This is a simple step that can make a real difference.

5. Overlooking Spousal and Survivor Benefits

I’ll admit—I didn’t fully understand how spousal benefits worked at first.

And that’s a big one, especially for married couples.

What I learned:

- Your spouse may be entitled to benefits based on your record

- Survivor benefits can be significantly higher than what you expect

- Timing strategies matter a lot here

This is an area where a little knowledge can go a long way—and potentially add thousands over time.

6. Missing the Bigger Retirement Income Picture

My biggest mistake? Looking at Social Security in isolation.

At first, I treated it like “extra income.” But it’s much more than that—it’s a foundational part of your retirement plan.

What I learned:

- Social Security should be coordinated with:

-

- Retirement accounts

- Retirement Taxes

- Medicare

- The timing of when you claim affects everything else

Once I started looking at the full picture, things finally began to make more sense.

From Someone Who Learned the Hard Way

If there’s one thing I want you to take away from this—it’s this:

Don’t rush your Social Security decisions.

Take your time. Learn how the system works. And most importantly, think about how your choices today will impact your income for the rest of your life.

I made some of these mistakes so you don’t have to.

Step-by-Step Guide to Getting the Most From Your Social Security

Discover How To Avoid Social Security Mistakes

If I could sit down with you one-on-one and walk you through this, here’s exactly what I’d tell you to do—step by step.

Step 1: Know Your Full Retirement Age (FRA)

Before you make any decisions, you need to know your Full Retirement Age.

Why this matters:

- This is the age you qualify for your full benefit

- Claiming before this reduces your income

- Claiming after this increases your benefit

Jeffs Tip:

- If you were born between 1943–1960, your FRA is between 66 and 67

This is your starting point for everything.

Step 2: Create Your Social Security Account

If you haven’t done this yet, do it first—seriously.

Go to the official SSA website and:

- Create your account

- Review your estimated benefits

- Check your earnings history

Why this step is critical:

This is where I wish I had started earlier. You can’t plan properly if your numbers are wrong.

Step 3: Verify Your Earnings Record

This step is simple—but incredibly important.

What to look for:

- Missing years of income

- Incorrect earnings amounts

Why it matters:

Your benefit is calculated based on your highest 35 years of earnings. Errors here = less money in your pocket.

Fixing this early can increase your future income.

Step 4: Decide When to Claim

Don’t Rush This

This is the biggest decision—and where most people (including me) slip up.

Your options:

- Age 62 → earliest (lower monthly benefit)

- Full Retirement Age → full benefit

- Age 70 → maximum benefit (thanks to delayed credits)

What I learned:

- Waiting increases your benefit roughly 8% per year after FRA

- That increase is permanent

Think about:

- Your health

- Your income needs

- Your life expectancy

- Whether you’re still working

There is no one-size-fits-all answer—but there IS a right answer for you.

Step 5: Understand the “Working While Collecting” Rules

How To Find Work From Home Jobs For Seniors

If you plan to work while collecting benefits, don’t skip this.

Here’s the deal:

- If you’re under FRA, income limits apply

- Earn too much → your benefits may be reduced (temporarily)

The good news:

- Once you reach FRA, those limits disappear

- You may get credit back later

This is one of those “surprise mistakes” I wish I had avoided.

Step 6: Plan for Taxes

A lot of retirees don’t see this coming—I didn’t either.

What to know:

- Social Security isn’t always tax-free

- Up to 85% of your benefits can be taxable depending on your income

What to do:

- Look at all income sources together:

-

- Social Security

- Retirement withdrawals

- Part-time work

- Consider tax-efficient withdrawal strategies

A little planning here can save you a lot later.

Step 7: Don’t Overlook Spousal & Survivor Benefits

If you’re married (or were), this is HUGE.

What many people miss:

- You may qualify for up to 50% of your spouse’s benefit

- Survivor benefits can be even higher

Strategy matters:

- Who claims first

- When each spouse claims

This is one of the most overlooked ways to maximize lifetime income.

Step 8: Coordinate Social Security With Your Retirement Plan

This is where everything comes together.

Don’t treat Social Security as “extra money”

Instead, align it with:

- Your retirement savings

- Required withdrawals (RMDs)

- Healthcare costs (Medicare)

- Tax strategy

What I learned:

Once I looked at everything together, my decisions became much clearer—and smarter.

Step 9: Revisit Your Plan Every Year

Your situation will change—and your strategy should too.

Review annually:

- Income needs

- Tax situation

- Health changes

- Work status

Even small adjustments can make a big difference over time.

Consider This

If I could sum this up in one sentence:

The biggest Social Security mistakes happen when we make quick decisions without a plan.

Take your time. Understand your options. And think long-term.

That’s how you turn Social Security into a powerful, reliable income stream—not a missed opportunity.

Top-Rated Social Security Books on Kindle Unlimited

Best Kindle Ebooks For Retirement Income Guide

A Quick Note About the Kindle Unlimited Ebooks I Share

You may notice that we occasionally recommend helpful ebooks within our articles.

Many of these titles are available free to read for Kindle Unlimited members as part of their subscription. When readers choose to read these included ebooks through Kindle Unlimited, I do not earn any commissions from any free purchases only ifyou decide to order a paid version.

We share these resources because I believe they can be genuinely helpful

- Social Security Planning

- Maximizing Your Social Security Benefits

- Medicare & Social Security Made Simple

Why Kindle Unlimited Can Be a Smart, Budget-Friendly Choice

When you’re living on a fixed or semi-fixed income, every dollar matters. I’ve learned that the little monthly expenses can either drain your budget—or actually give you a lot of value in return.

That’s exactly how I look at Kindle Unlimited.

At first, I wasn’t sure if it was worth paying for another subscription. But after using it, I realized it can be one of the most cost-effective ways to enjoy reading, learning, and even entertainment—without constantly buying new books.

Access to Thousands of Books Without Paying Per Book

One of the biggest benefits is simple:

You don’t have to buy every book you want to read.

With Kindle Unlimited, you get access to:

- Thousands of eBooks

- Audiobooks (on select titles)

- Magazines

Why this matters:

If you’re used to paying $10–$20 per book, it doesn’t take long for this membership to pay for itself.

A Budget-Friendly Way to Keep Learning and Stay Entertained

Affordable Kindle eBook & Deals

In retirement, staying mentally active is just as important as staying financially secure.

What I like about it:

- You can explore new topics without risk

- Try books you wouldn’t normally buy

- Drop a book if you don’t like it—no money wasted

Whether it’s:

- Retirement planning

- Health and wellness

- Health Tips for Senior Dog Owners

- Or just a must-read best sellers

…it’s all right there.

Unlimited Reading = More Value for Your Money

Here’s where it really stands out.

- You can borrow multiple books at a time

- Return them anytime

- Borrow more as often as you want

It’s kind of like having a digital library—but without waiting lists.

From my experience:

Even reading just 1–2 books a month can make the membership worth it. Sign up for the free trial as I did to see if this is worth you becoming a member first, what I found out during my free trial I more free ebooks that I realized I would have.

Great for Lifelong Learning Without Breaking the Bank

A lot of retirees want to:

- Learn new skills

- Start hobbies

- Dive deeper into topics they never had time for

This gives you that opportunity—without constantly spending money.

Think of it as:

A low-cost way to invest in yourself.

My Honest Experience

I’ll be upfront—Kindle Unlimited isn’t perfect for everyone.

It’s a great fit if you:

- Enjoy reading regularly

- Like exploring different topics

- Want to save money on books

It may not be ideal if:

- You only read occasionally

- You prefer only brand-new bestseller releases

But for me, and for many people trying to stretch their retirement dollars, it’s been a solid value.

Jeff Shares

When you’re managing retirement income, smart choices aren’t always about cutting back—they’re about getting more value for what you spend.

Kindle Unlimited is one of those small monthly expenses that can actually give you a lot in return.

Amazon Disclosure: As an Amazon Associate, I earn from qualifying purchases. Any Amazon links used throughout this website may earn a commission when you purchase through them.

Learn From My Mistakes Not Your Own

If there’s one thing I’ve learned through all of this, it’s that Social Security isn’t something you want to “wing.”

The decisions you make—when to claim, how to coordinate with your other income, and how much you understand the rules—can impact your finances for the rest of your life.

I made a few of these mistakes myself. Nothing catastrophic—but enough to realize how important it is to slow down, do a little homework, and think long-term.

The good news?

You don’t have to be perfect—you just have to be informed.

Take the time to:

- Understand your options

- Look at the big picture

- And make decisions that fit your situation—not someone else’s

Because when you get this right, Social Security becomes more than just a monthly check… it becomes a reliable foundation for your retirement.

And that’s what we’re all after, peace of mind and financial confidence in the years ahead.

Thank you for taking the time to read ” What Are Common Social Security Mistakes”

Jeff

Amazon Disclosure: As an Amazon Associate, I earn from qualifying purchases. Any Amazon links used throughout this website may earn a commission when you purchase through them.

12 Month Retirement Income Content Plan

- How To Improve Writing Skills Using Technology ResourcesHow to improve writing skills using technology resources. Many new writers lack the knowledge of the technology resources on the internet to use, so that is what I am going to provide you in the article that you are about to read. Affiliate Disclosure Amazon + Friends Affiliate Disclosure: Some of the links on this … Continue reading “How To Improve Writing Skills Using Technology Resources”

- How To Automate Facebook Group Content Posting With AIHow to automate FaceBook group content posting with AI is what you will learn from me. Many of you are more likely uising Facebook to promote your writing, no matter if you are writing blog articles or writing an ebook this something you will want to learn. Affiliate Disclosure Amazon + Friends Affiliate Disclosure: Some … Continue reading “How To Automate Facebook Group Content Posting With AI”

- 10 Best Kindle Unlimited Ebooks For Aspiring Authors10 best Kindle Unlimited eBooks for aspiring authors is a good resource for aspiring authors. By me doing the work for you, this saves you time from reading ebooks that are not the best resources for you. Affiliate Disclosure Amazon + Friends Affiliate Disclosure: Some of the links on this website may be affiliate links. … Continue reading “10 Best Kindle Unlimited Ebooks For Aspiring Authors”

- Where Can I Find Paid Writing Gigs In 2026 OnlineWhere can I find paid writing gigs in 2026 onliine to supplement your income. Many new writers lack the knowledge of where to find writing gigs, and how to find them on their own. In this article, you will learn where you can find opportunities that you might not be aware of. Affiliate Disclosure Amazon … Continue reading “Where Can I Find Paid Writing Gigs In 2026 Online”

- What Are The Top Ebooks For Writers In 2026 To ReadWhat are the top eBooks for writers in 2026 to read are good resources to know about. Many writers don’t take advantage of the eBooks that can provide them with a ton of valuable information, you will find the best eBooks for writers are writen by successful writers. Affiliate Disclosure Amazon + Friends Affiliate Disclosure: … Continue reading “What Are The Top Ebooks For Writers In 2026 To Read”

- How To Write A Special Ebook Step By Step GuideHow to write a special eBook step by step guide will amaze you how easy this really is, helping you accomplish this and your other writing goals is the mission of Boomer Biz HQ. Be sure to check all my step-by-step guides waiting to help you, now are you ready to write that special eBook. … Continue reading “How To Write A Special Ebook Step By Step Guide”

- 12 Top Writing Resources For New Writers Success In 202612 top writing resources for new writers success in 2026. With artificial intelligence 2026 has more to offer new writers success than ever before, interested in the 12 top writing resources for new writers, that is what I have to share with you in this article. Affiliate Disclosure Amazon + Friends Affiliate Disclosure: Some of … Continue reading “12 Top Writing Resources For New Writers Success In 2026”

- 10 Best Writing Productivity Tips For 202610 best writing productivity tips for 2026. Anyone at any age can be a productive writer, many seniors after they retire supplement their income by writing online. With my 10 best writing productivity tips you also can become a writer, why not take the first step right now. Affiliate Disclosure Amazon + Friends Affiliate Disclosure: … Continue reading “10 Best Writing Productivity Tips For 2026”

- How To Be A Productive Writer In 2026 For BeginnersHow to be a productive writer in 2026 for beginners. It is never too late to get your feet wet as a writer, many seniors have started writing productive without any prior experience. My beginner-friendly guide will help you get started on the right path. Affiliate Disclosure Amazon + Friends Affiliate Disclosure: Some of the … Continue reading “How To Be A Productive Writer In 2026 For Beginners”

- Writing Groups On Linkedin For 2026 To JoinWriting groups on Linkedin for 2026 to join is what you will learn. How many of you are using Linkedin, and how many of you are taking advantage of their writing groups. Many people miss out by not using Linkedin for a writing resource, so I am going to help you find groupls for 2026 … Continue reading “Writing Groups On Linkedin For 2026 To Join”

This was a really helpful read. I’m not retired yet, but Social Security is something I’ve been paying a lot more attention to as I get older, and articles like this are exactly why. It’s easy to assume you’ll just figure it out when the time comes, but the mistakes you shared make it clear that a lot of these decisions really need to be thought through ahead of time.

The part about claiming too early without a plan really stood out to me. I think a lot of people probably see 62 and assume that’s automatically the best move, without realizing how much it can affect long-term income. The taxes side is another one I’ve heard catches people off guard.

What I appreciate most is that you wrote this from real experience, not just theory. That makes it a lot more relatable and useful for people who are trying to avoid expensive mistakes later on.

Thank you Jason

Many people might not realize including you that if you start collecting social security at 62 you are going to receive one-third less than if you work longer.

Jeff